Live Preview (Coming Soon)

Eco-Addis Mobile — Super App for Addis Ababa

Title

Eco-Addis — A super-app for e-commerce, food delivery and ride-hailing in Addis Ababa

My Role

Lead UX/UI Designer

Team

1 Product Manager, 1 UI Designer, 1 UX Researcher, 2 Developers

Timeline

5 Months

Project Type

Personal / Client

Tools Used

Figma, FigJam, Google Forms, Maze

Problem Statement

Addis Ababa's rapidly growing urban population faces fragmented digital commerce experiences — separate apps for shopping, food delivery, and transportation. Vendors lack affordable digital storefronts, while consumers juggle multiple platforms with inconsistent UX. Eco-Addis was designed to solve this with a single, unified super-app ecosystem tailored specifically to Addis Ababa's urban lifestyle — supporting Ethiopian Birr (ETB), Amharic context, and local business categories.

Users & Pain Points

Who are the users?

Urban Addis Ababa residents aged 18–40 — students, professionals, and small business owners who are mobile-first consumers.

What are their goals?

Shop for products, food, and services in one place|Find nearby restaurants and get food delivered quickly|Order affordable rides without switching apps|Sell products or run a vendor shop digitally|Discover local businesses through video and stories

Pain points

•

No single app serving e-commerce, food delivery, and rides in the Ethiopian market|Existing global apps (Jumia, Uber) lack local language support and local business inventory|Small vendors have no accessible digital storefront|Currency and payment flows are not localized (no ETB, no local delivery logic)|Distrust of complicated onboarding — users drop off before first purchase

•

Disputes over draw fairness — no verifiable random selection

•

No single place to view contribution history, remaining rounds, or upcoming draws

•

Organizers overwhelmed managing payments and member communications manually

•

No formal way to submit a cancellation or special request

No single app serving e-commerce, food delivery, and rides in the Ethiopian market|Existing global apps (Jumia, Uber) lack local language support and local business inventory|Small vendors have no accessible digital storefront|Currency and payment flows are not localized (no ETB, no local delivery logic)|Distrust of complicated onboarding — users drop off before first purchase

"I want to see my payment history and the draw results in one place — not scroll through a WhatsApp group."

Process & Methods

Goals

Understand how Addis Ababa residents currently shop, eat, and travel — and where digital tools fail them

Methods

•

User interviews with Addis residents across income groups|Competitor analysis: Jumia Ethiopia, ride apps, informal WhatsApp commerce|Card sorting to determine navigation structure for a multi-service app|Contextual inquiry at local markets and food spots (Bole, Saris, Merkato)

Key Findings & Insights

Users strongly prefer a single app over switching — super-app model validated|ETB pricing and Amharic map labels are trust signals, not just nice-to-haves|Flash deals and time-limited offers drive impulse purchases in food delivery|Vendors want easy onboarding — category/subcategory industry selection must be simple|Social features (stories, video Watch tab) increase time-in-app and discovery|Ride-hailing users want saved frequent destinations and trip history at a glance

Final Solution

→

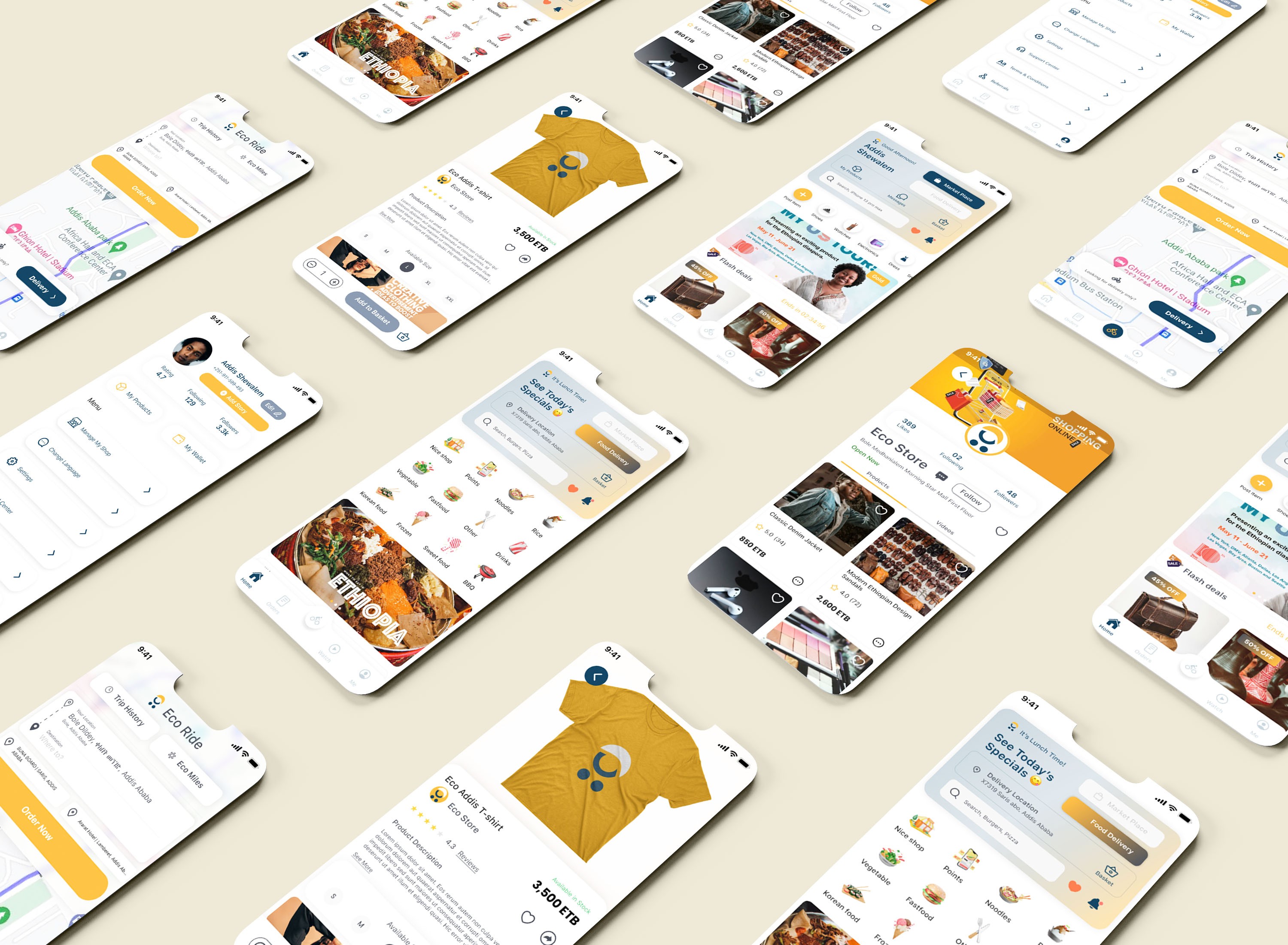

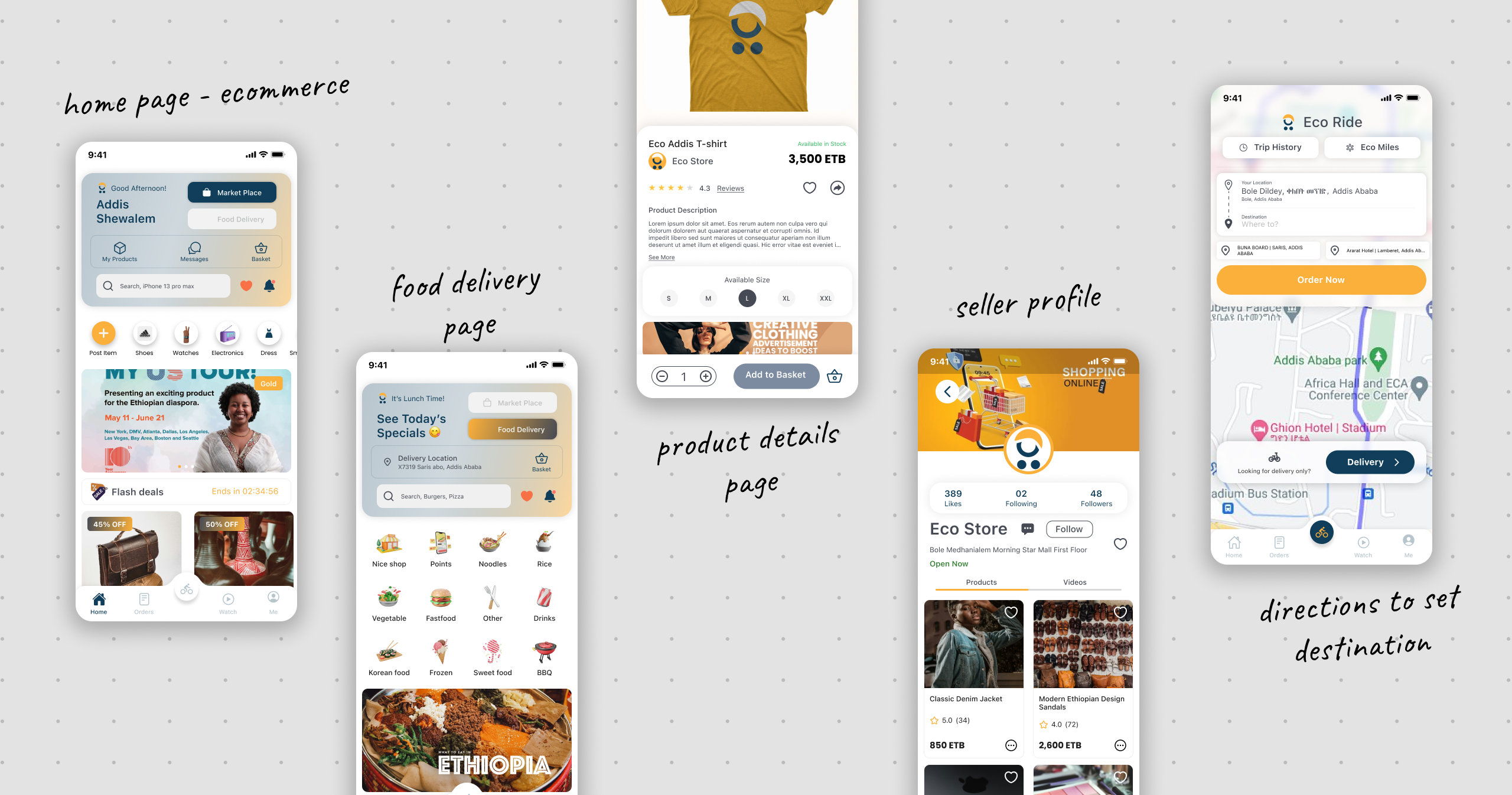

A clean locally-rooted mobile super-app with five core verticals: Market Place (product discovery, vendor shops, wishlist, reviews, flash deals); Food Delivery (restaurant pages, special offers, basket, checkout, order tracking); Eco Ride (map-based ride ordering, delivery mode, trip history, Eco Miles loyalty); Watch (vertical video feed for business promotion and discovery); and Me (user profile, my products, wallet, shop management, referrals). Design uses amber/golden yellow primary, dark navy secondary, ETB currency throughout, and real Addis Ababa addresses and Amharic map context.

Impact / Results

•

Onboarding completion rate target: >80%|Time to first order target: <3 minutes|Task success rate (find and add item to cart) target: >90%|Vendor registration completion target: >70%|SUS Score target: >80

Lessons Learned

Designing a super-app requires ruthless information architecture — the hardest challenge was keeping five product verticals discoverable without overwhelming the home screen|Localization is a UX feature not an afterthought — real Addis Ababa streets, ETB pricing, and Ethiopian food context in banners built immediate trust|Social commerce is underutilized in African markets — the Watch tab and Stories features were strong discovery and retention mechanisms|Vendors are users too — the vendor registration and boost flows needed as much design care as the consumer-facing shopping experience

© 2026 Nahom Girma. Designed & Hosted with 🦾 on

Live Preview (Coming Soon)

Eco-Addis Mobile — Super App for Addis Ababa

Title

Eco-Addis — A super-app for e-commerce, food delivery and ride-hailing in Addis Ababa

My Role

Lead UX/UI Designer

Team

1 Product Manager, 1 UI Designer, 1 UX Researcher, 2 Developers

Timeline

5 Months

Project Type

Personal / Client

Tools Used

Figma, FigJam, Google Forms, Maze

Problem Statement

Addis Ababa's rapidly growing urban population faces fragmented digital commerce experiences — separate apps for shopping, food delivery, and transportation. Vendors lack affordable digital storefronts, while consumers juggle multiple platforms with inconsistent UX. Eco-Addis was designed to solve this with a single, unified super-app ecosystem tailored specifically to Addis Ababa's urban lifestyle — supporting Ethiopian Birr (ETB), Amharic context, and local business categories.

Users & Pain Points

Who are the users?

Urban Addis Ababa residents aged 18–40 — students, professionals, and small business owners who are mobile-first consumers.

What are their goals?

Shop for products, food, and services in one place|Find nearby restaurants and get food delivered quickly|Order affordable rides without switching apps|Sell products or run a vendor shop digitally|Discover local businesses through video and stories

Pain points

•

No single app serving e-commerce, food delivery, and rides in the Ethiopian market|Existing global apps (Jumia, Uber) lack local language support and local business inventory|Small vendors have no accessible digital storefront|Currency and payment flows are not localized (no ETB, no local delivery logic)|Distrust of complicated onboarding — users drop off before first purchase

•

Disputes over draw fairness — no verifiable random selection

•

No single place to view contribution history, remaining rounds, or upcoming draws

•

Organizers overwhelmed managing payments and member communications manually

•

No formal way to submit a cancellation or special request

No single app serving e-commerce, food delivery, and rides in the Ethiopian market|Existing global apps (Jumia, Uber) lack local language support and local business inventory|Small vendors have no accessible digital storefront|Currency and payment flows are not localized (no ETB, no local delivery logic)|Distrust of complicated onboarding — users drop off before first purchase

"I want to see my payment history and the draw results in one place — not scroll through a WhatsApp group."

Process & Methods

Goals

Understand how Addis Ababa residents currently shop, eat, and travel — and where digital tools fail them

Methods

•

User interviews with Addis residents across income groups|Competitor analysis: Jumia Ethiopia, ride apps, informal WhatsApp commerce|Card sorting to determine navigation structure for a multi-service app|Contextual inquiry at local markets and food spots (Bole, Saris, Merkato)

Key Findings & Insights

Users strongly prefer a single app over switching — super-app model validated|ETB pricing and Amharic map labels are trust signals, not just nice-to-haves|Flash deals and time-limited offers drive impulse purchases in food delivery|Vendors want easy onboarding — category/subcategory industry selection must be simple|Social features (stories, video Watch tab) increase time-in-app and discovery|Ride-hailing users want saved frequent destinations and trip history at a glance

Final Solution

→

A clean locally-rooted mobile super-app with five core verticals: Market Place (product discovery, vendor shops, wishlist, reviews, flash deals); Food Delivery (restaurant pages, special offers, basket, checkout, order tracking); Eco Ride (map-based ride ordering, delivery mode, trip history, Eco Miles loyalty); Watch (vertical video feed for business promotion and discovery); and Me (user profile, my products, wallet, shop management, referrals). Design uses amber/golden yellow primary, dark navy secondary, ETB currency throughout, and real Addis Ababa addresses and Amharic map context.

Impact / Results

•

Onboarding completion rate target: >80%|Time to first order target: <3 minutes|Task success rate (find and add item to cart) target: >90%|Vendor registration completion target: >70%|SUS Score target: >80

Lessons Learned

Designing a super-app requires ruthless information architecture — the hardest challenge was keeping five product verticals discoverable without overwhelming the home screen|Localization is a UX feature not an afterthought — real Addis Ababa streets, ETB pricing, and Ethiopian food context in banners built immediate trust|Social commerce is underutilized in African markets — the Watch tab and Stories features were strong discovery and retention mechanisms|Vendors are users too — the vendor registration and boost flows needed as much design care as the consumer-facing shopping experience

© 2026 Nahom Girma. Designed & Hosted with 🦾 on

Live Preview (Coming Soon)

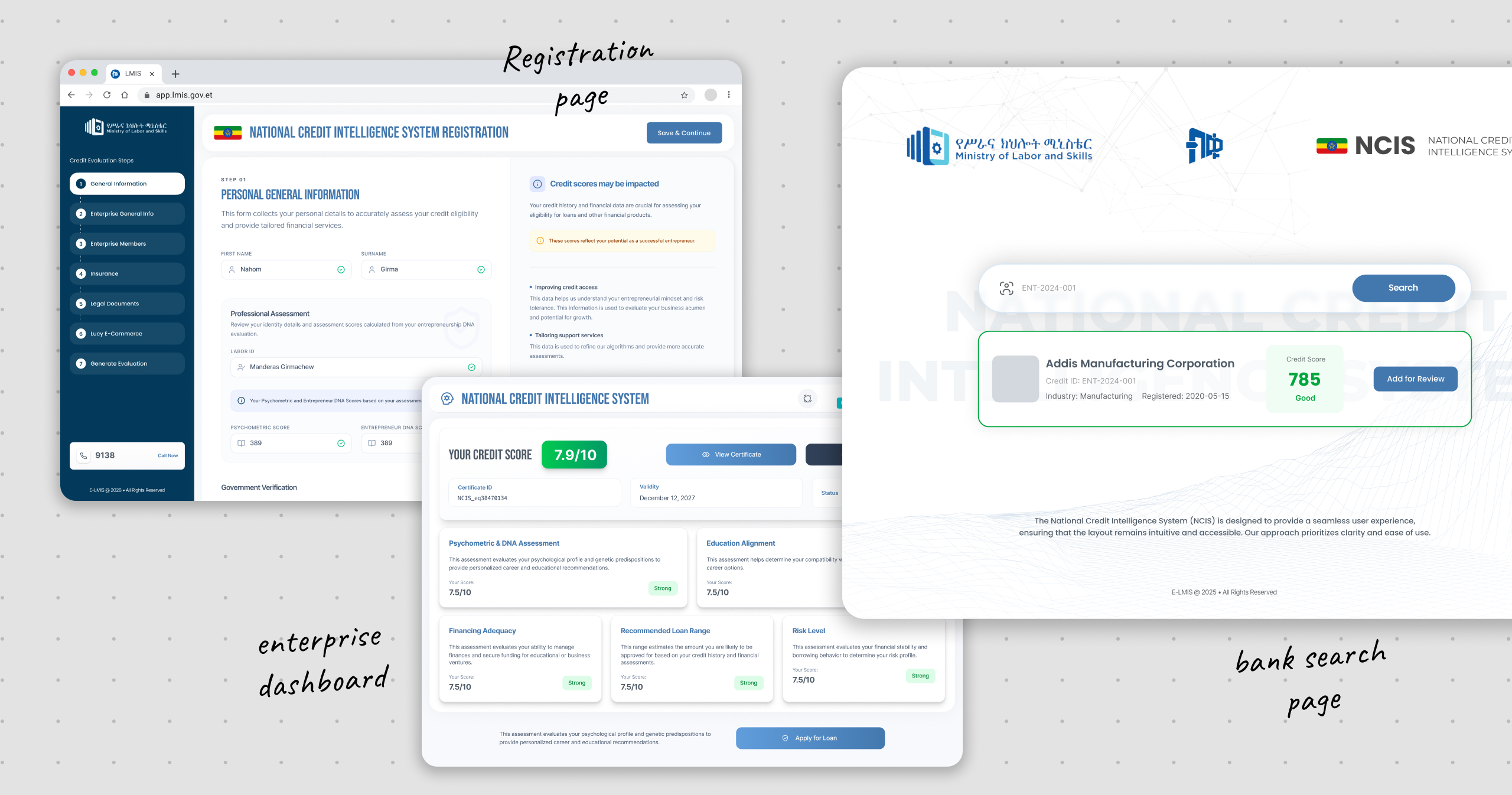

NCIS — National Credit Intelligence System

Title

NCIS — National Credit Intelligence System

My Role

Lead UI/UX Designer

Team

Nahom Girma (Designer)

Timeline

3 Weeks

Project Type

Government / Enterprise

Tools Used

Figma, NCIS Limited Design System v1.0.0

Problem Statement

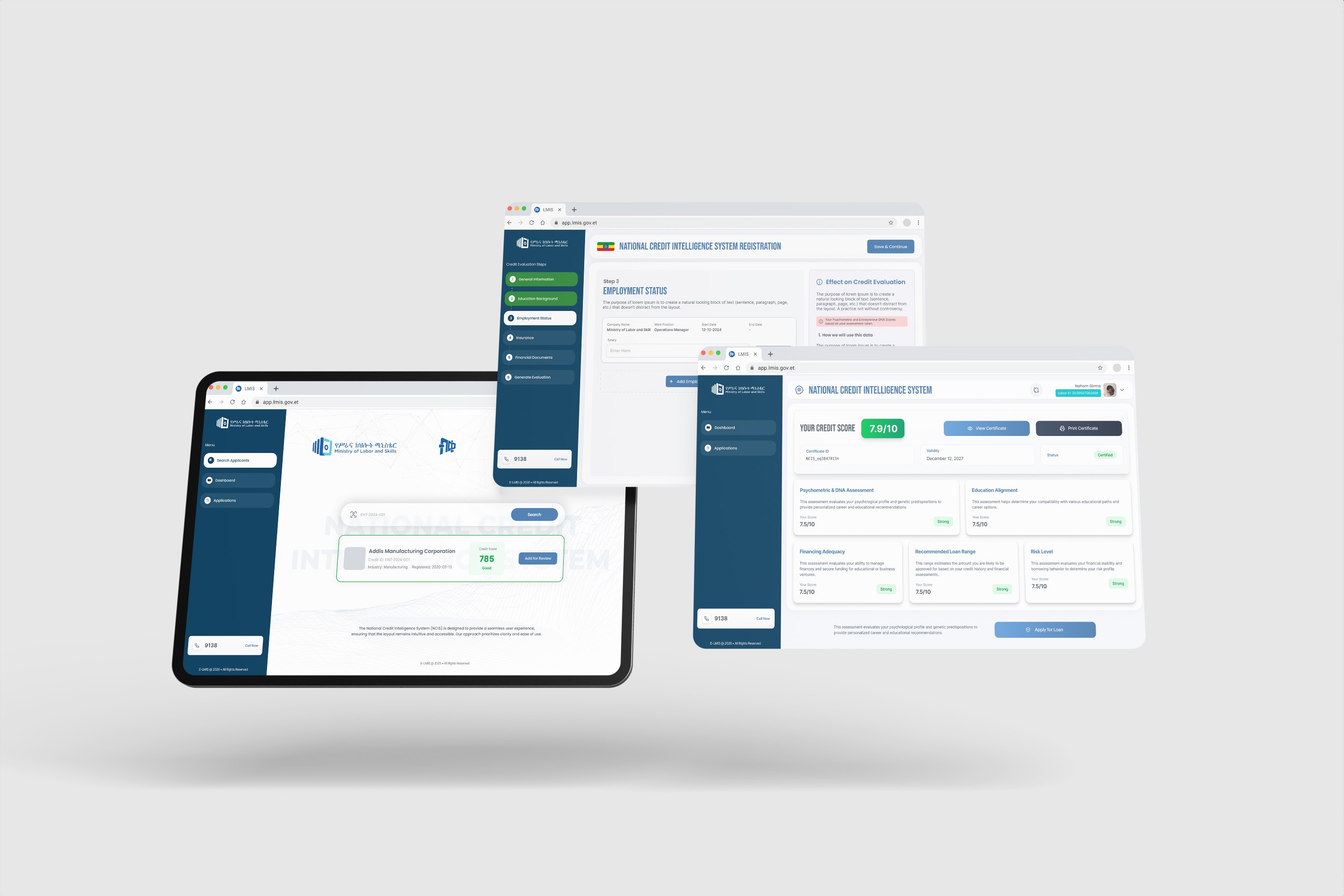

Ethiopia's informal economy — made up of micro-enterprises, sole traders, and unregistered businesses — has historically been locked out of formal financial services. Without a standardized credit history, verification system, or risk scoring mechanism, banks cannot lend to them, insurance companies cannot serve them, and government programs cannot track them. At the same time, formal enterprises also lacked a unified, trusted digital certificate of creditworthiness. The challenge was to design a national-scale credit intelligence platform that evaluates and scores creditworthiness across enterprise, personal, and informal sector applicants; bridges the gap between the E-LMIS labor identity infrastructure and financial services; and generates verifiable official credit certificates recognized by banks and government.

Users & Pain Points

Who are the users?

Six user types: Enterprise Applicants, Personal Applicants, Informal Sector Applicants, Bank Officers, Insurance Officers, and Government/Admin users.

What are their goals?

Get certified credit score and certificate to access loans|Evaluate creditworthiness across enterprise and personal applicants|Review loan and insurance applications efficiently|Monitor national credit analytics and equity across regions|Access formal financial services through a standardized evaluation

Pain points

•

Informal sector businesses locked out of formal credit due to lack of financial records|No unified digital certificate of creditworthiness for formal enterprises|Banks lack a trusted decision-making interface for credit assessment|No audit trail or transparency in loan and insurance decisions •No mobile option for quick field credit lookups

•

Disputes over draw fairness — no verifiable random selection

•

No single place to view contribution history, remaining rounds, or upcoming draws

•

Organizers overwhelmed managing payments and member communications manually

•

No formal way to submit a cancellation or special request

Informal sector businesses locked out of formal credit due to lack of financial records|No unified digital certificate of creditworthiness for formal enterprises|Banks lack a trusted decision-making interface for credit assessment|No audit trail or transparency in loan and insurance decisions •No mobile option for quick field credit lookups

"I want to see my payment history and the draw results in one place — not scroll through a WhatsApp group."

Process & Methods

Goals

Design a national-scale credit intelligence platform serving 6 user types|Bridge E-LMIS labor identity infrastructure with financial services|Generate QR-verifiable digital credit certificates|Streamline bank and insurer loan/insurance application review workflow|Provide government with real-time national credit analytics

Methods

•

Stakeholder analysis of Ministry of Labor and Skills requirements|Review of E-LMIS ecosystem and existing data infrastructure|Competitive analysis of credit intelligence platforms|Multi-role user flow mapping for 6 distinct user types

Key Findings & Insights

Informal sector businesses lack traditional financial records but have e-commerce transaction history (Lucy platform) as a creditworthiness signal|Psychometric and Entrepreneur DNA scoring extends credit evaluation beyond financial data|QR-verifiable digital certificate makes fraud extremely difficult and gives the certificate real-world credibility|Field agents need mobile quick-lookup without the full portal|Minimum character requirement on loan decline prevents lazy or discriminatory rejections

Final Solution

→

An end-to-end multi-role credit intelligence platform (30+ screens, 6 user types, full design system) with: a 7-step credit evaluation wizard; AI-brain visual identity; QR-verifiable Certificate of Credit Worthiness; bank and insurance officer portals with approve/decline workflows; government analytics dashboard (Power BI); and a mobile Enterprise Credit Check screen for field agents.

Impact / Results

•

96% approval-to-view ratio at launch (320/332)|Platform supports 30+ screens across 6 user roles|NCIS Limited Design System v1.0.0 published Feb 2026

Lessons Learned

The 7-step wizard turns complex data collection into a navigable, transparent journey|The Certificate of Credit Worthiness screen is the primary value output — it is the product|Designing for multiple applicant types within a single system without fracturing the experience is a major UX achievement|The contextual right-panel (Impact on Creditworthiness) at every wizard step is the most important UX trust-building mechanism|Lucy E-Commerce as a data signal is a locally-relevant and innovative credit indicator for informal businesses

© 2026 Nahom Girma. Designed & Hosted with 🦾 on